The banking sector is witnessing a significant transformation globally, and India is no exception. The rise of neo-banks—digital-only banks operating without physical branches—is challenging the established dominance of traditional banks, which have served as financial pillars for decades. While traditional banks rely on brick-and-mortar infrastructure, regulatory stability, and comprehensive financial services, neo-banks leverage technology, agility, and customer-centric digital experiences to attract a new generation of users. This juxtaposition has sparked debates on efficiency, security, accessibility, and long-term sustainability. Understanding the strengths, limitations, and societal implications of both banking models is crucial for policymakers, investors, and customers. This article provides a detailed 2000-word analysis of traditional banks versus neo-banks, exploring their benefits, challenges, arguments in favor and against, and concluding with strategic insights, while being SEO-friendly.

Understanding Traditional Banks and Neo-Banks

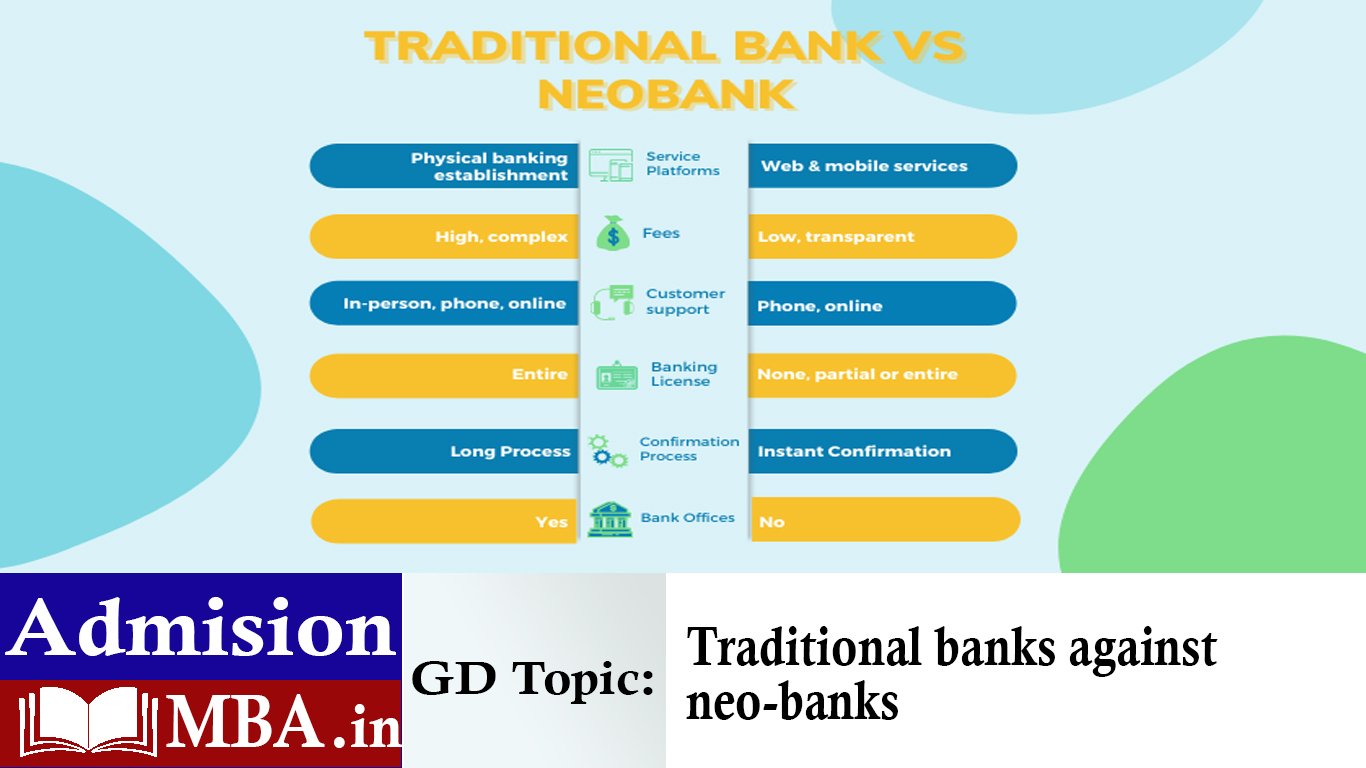

Traditional banks are financial institutions with a long-standing presence, operating through physical branches, ATMs, and a combination of online and offline services. They provide a wide range of services, including savings and current accounts, loans, credit facilities, investment products, insurance, and wealth management. Traditional banks are heavily regulated by central authorities such as the Reserve Bank of India (RBI), ensuring financial stability, deposit protection, and trust.

On the other hand, neo-banks are digital-only banking platforms that function without physical branches. They typically operate through mobile apps or web portals and rely on partnerships with traditional banks for core banking licenses. Neo-banks focus on enhancing customer experience, offering seamless account management, faster onboarding, real-time payments, and advanced analytics. Examples in India include Open, RazorpayX, Niyo, and Jupiter, while globally, companies like Chime and Revolut have set benchmarks in digital banking.

Advantages of Traditional Banks

1. Trust and Reliability

Traditional banks have established credibility over decades, with government backing and insured deposits, which enhances customer confidence.

2. Comprehensive Financial Services

They provide a wide range of services, including credit, insurance, investment, and wealth management, enabling customers to manage all financial needs under one roof.

3. Physical Presence and Accessibility

Branch networks and ATMs ensure physical accessibility, catering to customers who prefer in-person interactions or reside in semi-urban and rural areas.

4. Regulatory Oversight

Traditional banks operate under strict regulatory frameworks, ensuring financial stability, fraud protection, and adherence to compliance standards.

5. Creditworthiness and Lending Power

With higher capital reserves and established risk management frameworks, traditional banks can offer large-scale loans and corporate financing, supporting businesses and infrastructure projects.

6. Established Customer Base

They have long-term customer relationships, which facilitate personalized services and loyalty programs.

7. Financial Education

Through branch networks and advisory services, traditional banks contribute to financial literacy and awareness, particularly in rural and semi-urban regions.

8. Risk Management Expertise

Traditional banks have mature systems for credit scoring, fraud detection, and asset management, mitigating operational risks effectively.

9. Insurance and Deposit Protection

Customer deposits are typically insured under schemes like the Deposit Insurance and Credit Guarantee Corporation (DICGC), enhancing financial security.

10. Economic Stability

By channeling large-scale capital into infrastructure, industry, and government projects, traditional banks play a pivotal role in economic growth and stability.

Advantages of Neo-Banks

1. Superior Customer Experience

Neo-banks focus on user-friendly interfaces, quick onboarding, and 24/7 service, appealing to tech-savvy customers.

2. Cost Efficiency

With no physical branches, neo-banks reduce operational costs, allowing them to offer competitive fees, higher interest rates, or rewards.

3. Digital-First Innovation

Neo-banks provide real-time payments, automated bookkeeping, integrated financial analytics, and personalized notifications, enhancing financial management.

4. Quick Onboarding and Instant Services

Accounts can be opened within minutes digitally, with instant KYC verification, appealing to millennials and freelancers.

5. Integration with Fintech Ecosystem

Neo-banks integrate seamlessly with payment gateways, accounting software, and investment platforms, offering holistic financial solutions for businesses and individuals.

6. Transparency

With clear digital statements and fee structures, neo-banks enhance financial transparency.

7. Targeted Services for SMEs and Startups

Neo-banks provide customized business accounts, credit lines, and analytics for small and medium enterprises, often underserved by traditional banks.

8. Global Accessibility

Customers can access accounts anytime and anywhere, facilitating cross-border payments and global commerce.

9. Data-Driven Financial Insights

Neo-banks leverage AI and data analytics to provide personalized spending advice, budgeting tools, and cash flow forecasts.

10. Agility and Innovation

Without legacy systems, neo-banks adapt quickly to regulatory changes, technology trends, and customer feedback, maintaining competitive advantage.

Drawbacks of Traditional Banks

Slow digital adoption due to legacy systems and bureaucratic processes.

High operational costs from maintaining extensive branch networks.

Lengthy onboarding and approval processes for loans and accounts.

Limited customization for niche customer segments like freelancers or SMEs.

Lower engagement with tech-savvy users, who prefer digital-first experiences.

Complex fee structures and hidden charges.

Vulnerability to economic cycles, affecting profitability during downturns.

Slower innovation compared to fintech-driven solutions.

Geographical limitations in remote areas despite branches.

Dependence on physical infrastructure, which may not scale efficiently.

Drawbacks of Neo-Banks

Regulatory dependency on traditional banks for licenses and core banking infrastructure.

Limited services compared to full-service traditional banks.

No physical presence, which can alienate customers needing in-person support.

Data privacy and cybersecurity risks, given digital-first operations.

Profitability concerns, as many neo-banks operate at losses initially.

Limited lending power, especially for large corporate loans.

Potential exclusion of non-tech-savvy users, such as elderly or rural populations.

Operational risks due to dependence on technology and internet connectivity.

Overreliance on fintech partnerships, creating business dependencies.

Customer trust issues, as some users prefer insured, established institutions.

Arguments in Favor of Traditional Banks

Trust and reliability built over decades of operations.

Comprehensive financial services under one roof.

Regulated and stable, ensuring deposit protection.

Ability to provide large-scale credit for businesses and infrastructure.

In-person support and accessibility for rural and semi-urban populations.

Mature risk management and operational expertise.

Contribution to economic growth through investments and lending.

Financial literacy initiatives and advisory services.

Deposit insurance ensuring customer confidence.

Integration with government financial schemes and subsidies.

Arguments in Favor of Neo-Banks

Enhanced customer experience through intuitive digital platforms.

Cost-effective and transparent services for users.

Quick onboarding and instant account management.

Tailored services for SMEs, startups, and freelancers.

Integration with fintech and payment ecosystems.

Data-driven insights for smarter financial decisions.

Agility to adapt to regulatory changes and market trends.

Encourages digital adoption and innovation in banking.

Accessible anywhere, anytime, supporting global transactions.

Encourages competition leading to better financial products and services.

Societal and Economic Implications

1. Financial Inclusion

Neo-banks, through mobile-first platforms, can reach underbanked populations, complementing traditional banks’ efforts to promote financial inclusion.

2. Economic Efficiency

Digital banking reduces transaction costs, increases payment efficiency, and facilitates real-time business operations.

3. Technology-Driven Workforce

Neo-banks foster employment in tech, analytics, and digital services, while traditional banks sustain jobs in branch networks, customer service, and advisory roles.

4. SME Empowerment

Neo-banks provide tailored financial solutions for SMEs, encouraging entrepreneurship, cash flow management, and credit access.

5. Cybersecurity and Privacy Concerns

As financial operations digitize, both banking models must address data protection, fraud prevention, and secure digital payment mechanisms.

6. Competition and Innovation

The coexistence of traditional and neo-banks drives innovation, improves service quality, and benefits consumers with better products and lower fees.

7. Regulatory Adaptation

The rise of neo-banks requires updated regulatory frameworks, balancing innovation with financial stability and consumer protection.

8. Global Banking Trends

India’s adoption of neo-banks aligns with global digital banking trends, fostering cross-border payments and international investment opportunities.

9. Financial Literacy and Awareness

Digital platforms promote financial education through in-app analytics, spending insights, and personalized advice.

10. Economic Resilience

A diversified banking ecosystem combining traditional stability and neo-bank agility strengthens the financial system’s resilience against shocks and economic crises.

Strategies for Coexistence and Growth

Collaboration between neo-banks and traditional banks to leverage regulatory licenses and digital innovation.

Investment in cybersecurity to safeguard digital transactions and customer data.

Digital transformation in traditional banks to improve onboarding, user experience, and operational efficiency.

Financial literacy programs for users adapting to digital banking platforms.

Customized services for niche markets like SMEs, freelancers, and tech-savvy customers.

Regulatory frameworks to ensure competition, innovation, and consumer protection.

Encouraging fintech partnerships for technology integration and scalability.

Promoting financial inclusion in rural and underserved regions.

Data analytics and AI adoption for smarter lending and personalized financial services.

Long-term investment in human resources for both digital and traditional banking roles.

Conclusion

The debate between traditional banks and neo-banks reflects the evolving landscape of banking in India and globally. Traditional banks offer stability, regulatory oversight, comprehensive financial services, and physical presence, making them indispensable for economic growth, large-scale lending, and public trust. Conversely, neo-banks bring digital-first innovation, cost-efficiency, superior user experience, and agility, appealing to tech-savvy individuals, startups, and SMEs.

While traditional banks continue to dominate core banking services and capital-intensive operations, neo-banks are reshaping customer expectations, accelerating digital adoption, and promoting financial inclusion. The future of banking lies in a hybrid ecosystem where traditional banks leverage digital innovation and neo-banks gain regulatory credibility and stability through strategic partnerships.

In conclusion, traditional banks and neo-banks are not mutually exclusive but complementary. By integrating the strengths of both models, India can foster a robust, inclusive, and technologically advanced banking sector, supporting economic growth, financial inclusion, and innovation for decades to come.

As an experienced writer, AdmissionMBA is especially interested in small and medium-sized businesses (SMEs). He loves being able to give real steps that anyone can take right now to start making business better for everyone.