SWIFT and Global Banking System

The Society for Worldwide Interbank Financial Telecommunication (SWIFT) is often referred to as the backbone of the global financial system. Established in … Learn More..

Group discussion round is a favourite component of the final selection round not only in top MBA colleges but also in various recruitment processes like class 1 and 2 services, SSB, bank officers recruitment services. It also holds immense importance in the final admission/selection process. Group discussion rules also help you to speak effectively and listen to others.

MBA Admission Opportunity in MBA 2026-28 at Colleges/Universities

Colleges/Universities will accept above entrance exam score.

Apply Fill Form and call 11:00AM to 07:00 PM 011-41444275 Mobile No. 9811004275.

5000+ Seats in Top MBA Colleges in Top richest cities in India.

Tow Year MBA Fee between 4 to 16 lakh with average salary in Placement is Rs. 4 lakhs to 1 million.

The admission process of MBA in India usually consists of entrance examination and written aptitude test or essay writing, group discussion and personal interview.

The Society for Worldwide Interbank Financial Telecommunication (SWIFT) is often referred to as the backbone of the global financial system. Established in … Learn More..

The launch of 5G technology is being hailed as a revolutionary step in the world of telecommunications. Unlike previous generations of wireless … Learn More..

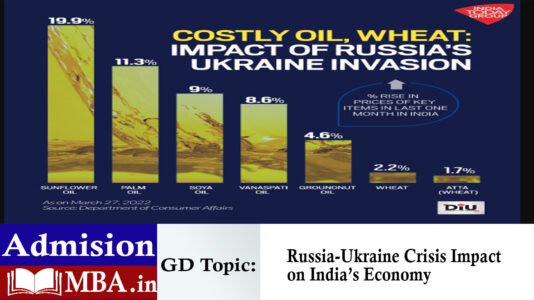

The Russia-Ukraine crisis, which began in February 2022, has had a profound impact not only on global geopolitics but also on economies … Learn More..

The term “Unicorn” was coined in 2013 by venture capitalist Aileen Lee to describe privately held startups valued at over $1 billion. … Learn More..

The Union Budget 2022-23, presented by Finance Minister Nirmala Sitharaman on 1st February 2022, came at a time when India was gradually … Learn More..

The concept of a cashless society has gained immense momentum in the last decade with the rise of digital payments, mobile wallets, … Learn More..

Currency exchange rates define the economic strength of nations. They influence trade, investments, tourism, remittances, and even geopolitical relations. The Indian rupee … Learn More..

The debate over whether people should invest in cryptocurrency has become one of the most polarizing discussions in the world of finance. … Learn More..

India is in the midst of a massive transformation in its infrastructure development strategy. To accelerate growth, improve logistics, and reduce costs … Learn More..

The Evergrande crisis has been one of the most significant financial shocks in recent years, raising alarm across global markets. China’s Evergrande … Learn More..