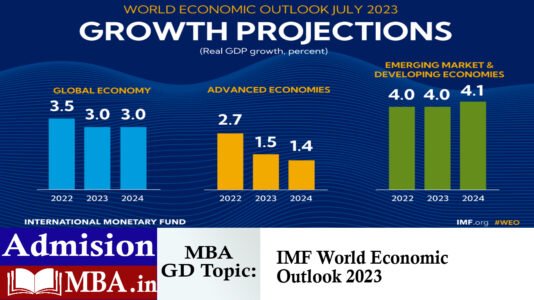

IMF World Economic Outlook 2023

The International Monetary Fund (IMF) World Economic Outlook (WEO) 2023 presents a detailed analysis of global economic trends, offering projections and policy … Learn More..

Group discussion round is a favourite component of the final selection round not only in top MBA colleges but also in various recruitment processes like class 1 and 2 services, SSB, bank officers recruitment services. It also holds immense importance in the final admission/selection process. Group discussion rules also help you to speak effectively and listen to others.

MBA Admission Opportunity in MBA 2026-28 at Colleges/Universities

Colleges/Universities will accept above entrance exam score.

Apply Fill Form and call 11:00AM to 07:00 PM 011-41444275 Mobile No. 9811004275.

5000+ Seats in Top MBA Colleges in Top richest cities in India.

Tow Year MBA Fee between 4 to 16 lakh with average salary in Placement is Rs. 4 lakhs to 1 million.

The admission process of MBA in India usually consists of entrance examination and written aptitude test or essay writing, group discussion and personal interview.

The International Monetary Fund (IMF) World Economic Outlook (WEO) 2023 presents a detailed analysis of global economic trends, offering projections and policy … Learn More..

Income inequality and poverty are two of the most pressing social and economic challenges facing the world today. Despite rapid economic growth … Learn More..

The fall of Credit Suisse, a globally significant financial institution, in March 2023, sent shockwaves through international markets and prompted a reevaluation … Learn More..

The Group of Seven (G7) is an intergovernmental economic organization consisting of Canada, France, Germany, Italy, Japan, the United Kingdom and the … Learn More..

The Goods and Services Tax (GST), implemented in India on 1st July 2017, represents one of the most significant tax reforms in … Learn More..

The transition to electric vehicles (EVs) has become a global priority due to climate change, urban pollution and energy security concerns. India, … Learn More..

The economic partnership between India and Japan has strengthened significantly over the past few decades, evolving from trade-centric engagement to strategic economic … Learn More..

In recent years, the Buy Now Pay Later (BNPL) model has revolutionized the way consumers make purchases. BNPL allows customers to buy … Learn More..

The collapse of Silicon Valley Bank (SVB) in March 2023 sent shockwaves across global financial markets, raising concerns about banking stability, venture … Learn More..

Artificial Intelligence (AI) and automation are transforming global industries, economies and societies. From self-driving cars and intelligent chatbots to automated manufacturing and … Learn More..